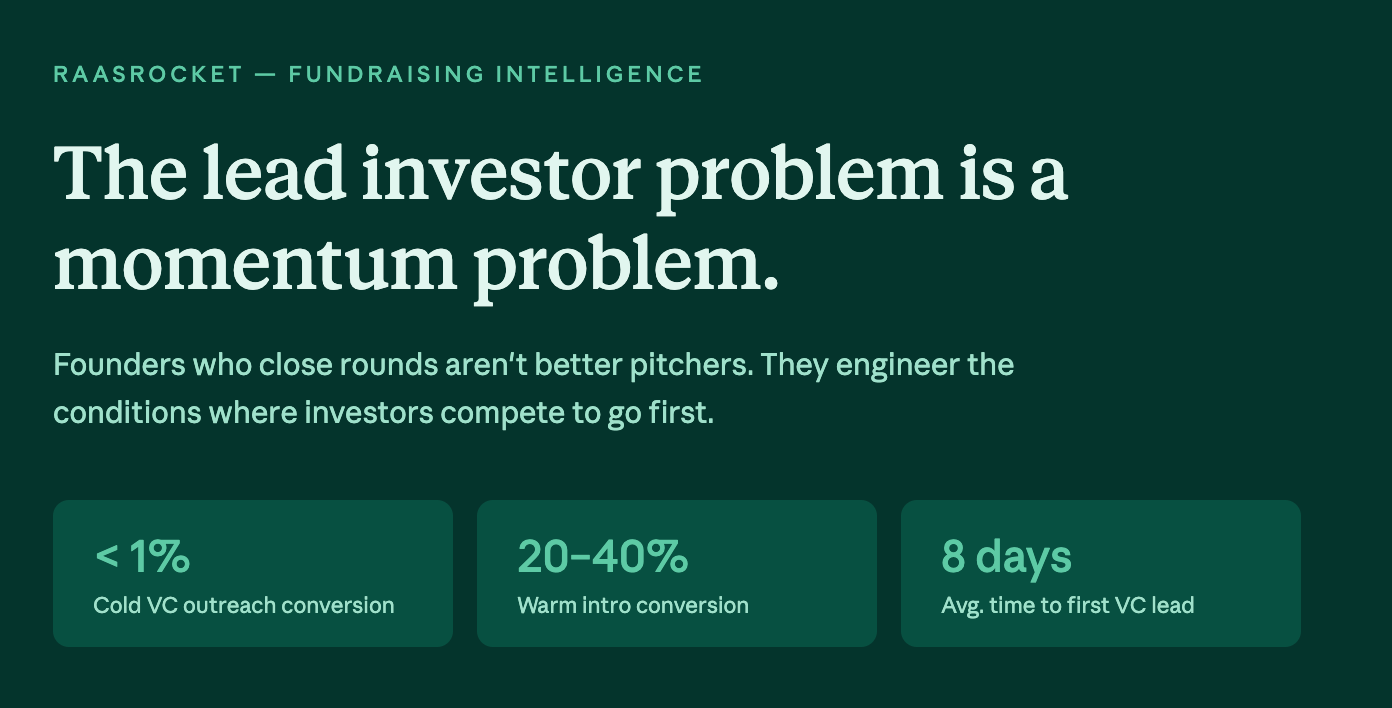

The Lead Investor Problem

And How to Engineer Your Way Out of It

I’ve watched hundreds of founders raise — or fail to raise — and the pattern is almost always the same.

They have a real company. Real traction. Real belief from investors in their conversations. And yet the round doesn’t close.

Not because they built the wrong thing.

Not because they pitched badly.

Because nobody would go first.

This is the lead investor problem. And it’s the single most common reason good companies don’t get funded.

What actually happens

Here’s how most seed rounds die.

A founder spends three months taking meetings. Investors say things like “we love the space” and “keep us posted on progress.” Some say “we’d love to participate” but nobody says “we’ll lead.”

The founder waits. They follow up. They get polite non-responses. And slowly, what felt like a room full of interested investors evaporates into silence.

This isn’t because the investors were lying. It’s because interest and conviction are different things.

Leading a round means setting terms, doing real diligence, writing a check before anyone else has, and staking your reputation on this company in front of your LPs. That’s a completely different ask from “being interested.”

Most investors will stay interested indefinitely. Very few will move first.

So the founder sits in investor purgatory — not rejected, not funded — burning runway while waiting for something that requires a trigger they don’t know how to create.

The real diagnosis

Here’s what almost nobody tells founders:

The lead investor problem is not a pitch problem.

It’s a momentum problem.

Investors don’t lead because they’ve been persuaded by a perfect deck. They lead because they’re afraid of missing something that’s already moving — and because the cost of not moving feels higher than the risk of going first.

The founders who close rounds fastest are not the best storytellers. They’re the ones who manufacture the conditions where waiting feels like a mistake.

That’s a completely different skill. And it’s learnable.

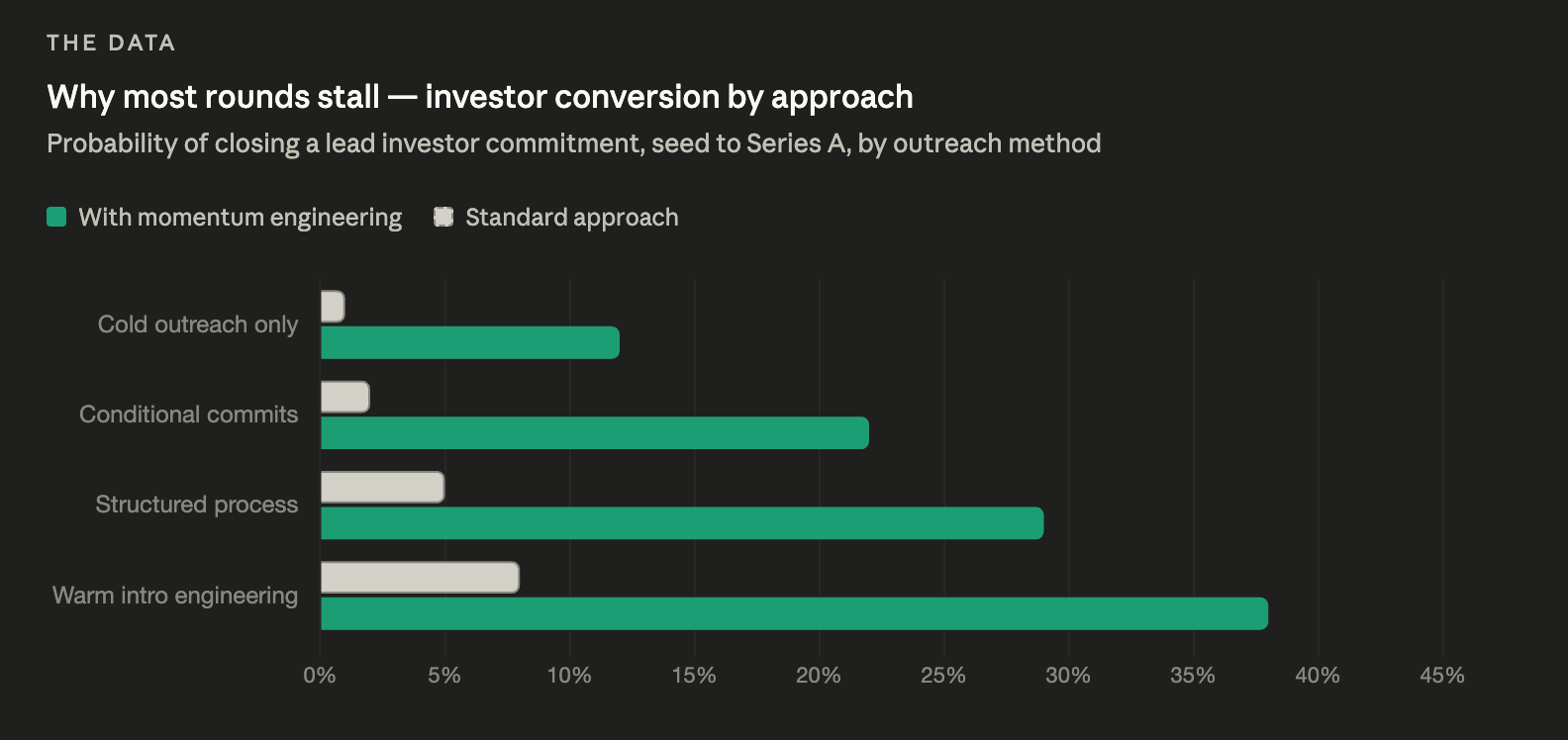

Three mechanisms that work

Over hundreds of fundraising campaigns at RaasRocket, we’ve identified the plays that actually solve the lead problem. Here are three.

1. The commitment cascade

Stop looking for a lead first.

Instead, go to 20-30 investors aligned with your thesis and ask one simple question: “If a lead closes, are you in?”

Soft commits. Conditional yeses. No pressure, no terms.

Collect $1-1.5M in conditional commitments.

Now go to your lead candidates with this framing: “I have $1.4M ready to close behind you. You set the terms, you get the best deal, and the round is essentially pre-filled. Your job is to lead a round that’s already won — not take a lonely first bet.”

You’ve completely changed the conversation. The lead’s risk just dropped by 80%. Their upside — best terms, pro-rata, board optionality — is fully intact. And they’re not going first into the dark. They’re leading a room that’s already full.

Most founders fail here because they don’t have the infrastructure to run a conditional commitment campaign. They don’t know which 30 investors to target, how to sequence the outreach, or how to collect soft commits without burning relationships. That’s exactly what we build at RaasRocket.

2. The structured process

Most founders pitch investors one at a time, sequentially, hoping one eventually leads. This is the slowest and least effective way to run a round.

Sophisticated founders run a process.

Set a close date. Tell every investor you approach that you’re running a 3-week lead selection process. Send a one-page process letter — not a deck, not a cold email — that signals you’re running a real transaction, not begging for a check.

Something like: “We’re running a structured lead selection process closing [date]. The lead sets terms and gets priority economics. We’re speaking with 8 firms. Happy to schedule time this week if this aligns.”

This creates urgency, filters out tourists, and reframes you from a founder asking for help to an operator running a process.

Investors who can’t decide in three weeks weren’t going to lead anyway. You just saved yourself six weeks of coffee chats that go nowhere.

3. The strategic lead

The most underused move in early-stage fundraising: the best lead investor for your round might not be a VC at all.

Corporate strategics — Salesforce Ventures, Google Ventures, Stripe, Shopify, HubSpot — write fast checks because their decision criteria is strategic, not purely financial. They’re buying access, optionality, and competitive intelligence. They also validate your thesis in a way no financial VC can.

The pitch to a strategic isn’t “here’s our financial return.” It’s: “This category is getting built with or without you. The question is whether you define it or react to it.”

Having a strategic lead unlocks VC followers immediately — every financial investor behind them reads it as: the incumbents already know this is coming.

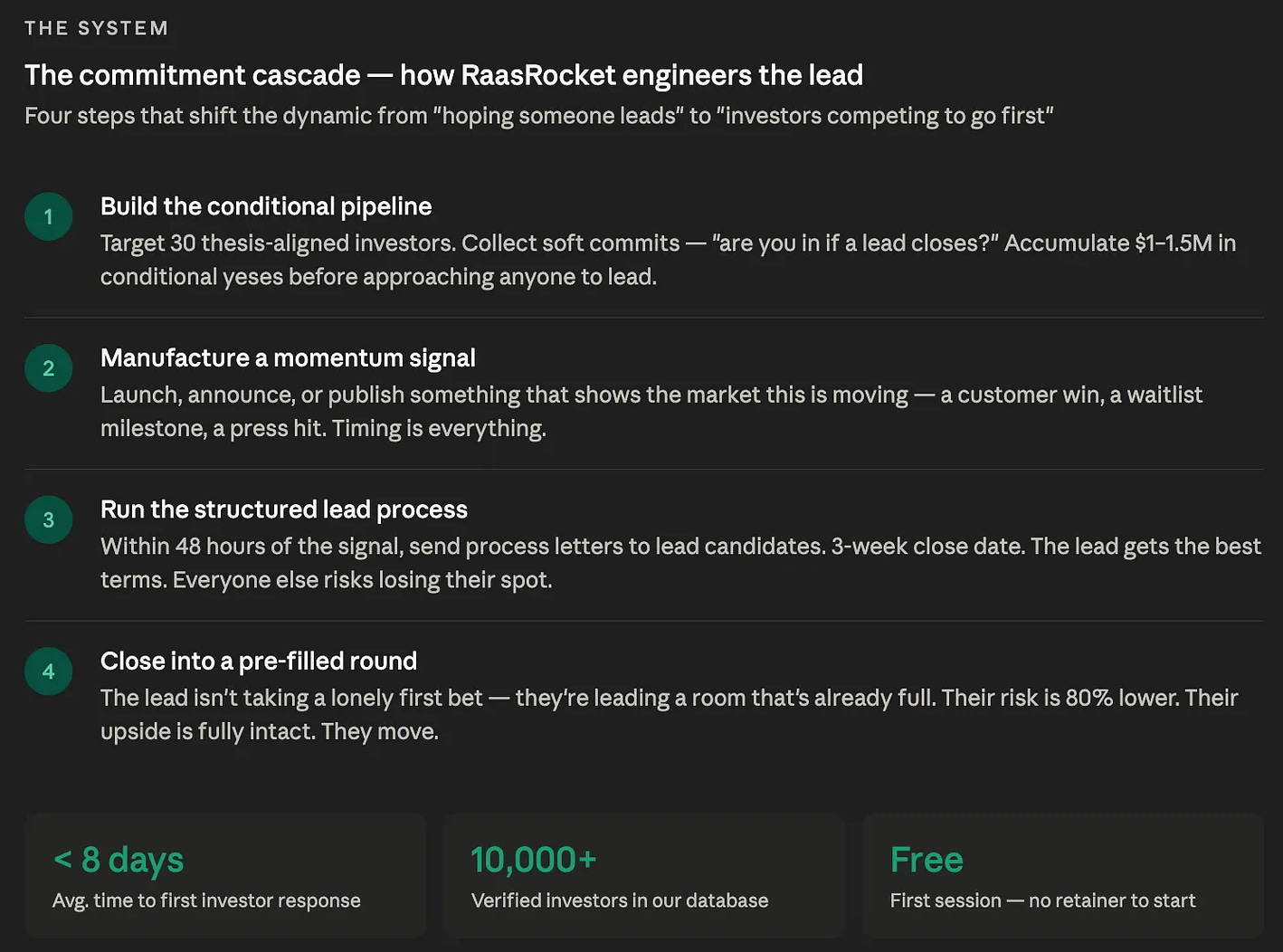

The combination play

Here’s how you put it all together.

Step one: build your conditional commitment pipeline. Identify 30 investors by thesis fit. Run soft commit outreach. Collect $1-1.5M in conditional yeses.

Step two: time a public momentum signal. A product launch, a customer announcement, a waitlist milestone, a press hit. Something that tells the market this is moving.

Step three: within 48 hours of the signal dropping, send your process letters to lead candidates. You have momentum, you have a pre-filled round, and you have a deadline.

Step four: the lead who moves first gets the best deal. Everyone else risks losing their spot.

You haven’t found a lead. You’ve manufactured the conditions where investors compete to be the lead.

Why almost nobody does this

Because it requires infrastructure most founders don’t have.

You need a targeted investor list built by thesis fit, not just name recognition. You need a conditional commitment outreach campaign that collects soft yeses without burning relationships. You need a structured process document that signals credibility. You need the timing coordination to hit the momentum signal and the lead outreach simultaneously.

Most founders try to run all of this manually, reactively, and alone. That’s why they stay in investor purgatory for six months while their runway disappears.

At RaasRocket, this is the entire system. We build and run the full lead engineering infrastructure — conditional commitment campaigns, structured process design, strategic lead identification, momentum timing — so founders stop waiting for a lead to appear and start engineering the conditions where leads compete.

Results typically begin in under 8 days from launch.

The market reality in 2026

VC round count hit a 6-year low in 2025, even as total dollars went up.

More money is chasing fewer deals. The founders getting funded aren’t necessarily building better companies. They’re running better processes.

The lead investor problem is solvable. But you have to treat it like the systems problem it is — not the social problem most founders assume it to be.

If you’re raising in the next 90 days and want to see how we’d engineer your lead, start at raasrocket.com. First session is free.

— Charles